U.S. Treasury's New Financial Surveillance Program Targets America's Border Communities

Is it a pilot program?

On a warm March afternoon, a woman stands outside a small storefront in San Ysidro, California, contemplating whether to enter. The purple and yellow Western Union sign in the window once represented her lifeline to family in Oaxaca—the means by which she sent part of her landscaping earnings to her mother and two children. Now it represents something else: risk.

She ultimately walks away, deciding not to send money today.

[Author's note: The opening scene describes a hypothetical situation. As the FinCEN order was just published on March 14, 2025, and will come into effect on April 13, 2025 (30 days after publication in the Federal Register), I have not yet documented specific cases but anticipate similar scenarios based on expert assessments of the policy's likely impacts.]

This scenario may soon become reality for many of the more than million residents in thirty ZIP codes along the Southwest border who now find themselves caught in an unprecedented financial dragnet.

On March 13, the Treasury Department's Financial Crimes Enforcement Network (FinCEN) issued a Geographic Targeting Order that dramatically lowers the threshold for currency transaction reports from ten thousand dollars to a mere two hundred dollars—an amount that captures virtually every meaningful money transfer across the border.

The ostensible target of this surveillance expansion is the flow of illicit funds tied to cartel activity. Trump’s Treasury Secretary Scott Bessent framed it as "whole-of-government approach to combatting the threat," saying Treasury "remains focused on leveraging all our available tools and authorities to better identify and counter these criminal activities." But immigration advocates, financial inclusion experts, and civil libertarians will undoubtedly view this as something much more troubling: a pilot program for a new kind of surveillance state that could eventually be deployed nationwide–and one that happens to align perfectly with the Trump administration's aggressive agenda of mass deportation.

The affected areas read like a tour of America's borderlands: Imperial and San Diego counties in California; Cameron, El Paso, Hidalgo, Maverick, and Webb counties in Texas:

These communities share certain qualities—proximity to Mexico, large immigrant populations, and economies that have long depended on the flow of people, goods, and money across the border. Now, they share something else: status as testing grounds for what may become the most sweeping expansion of financial surveillance in American history.

"Should criminals successfully tempt the United States to abandon the human right to privacy and the U.S. Constitution, everyone will lose," warned Fight for the Future in a 2023 letter to incoming lawmakers, a warning that seems especially prescient now that surveillance has been expanded to transactions as small as $200.

The mechanics of the order are technically complex, but practically straightforward.

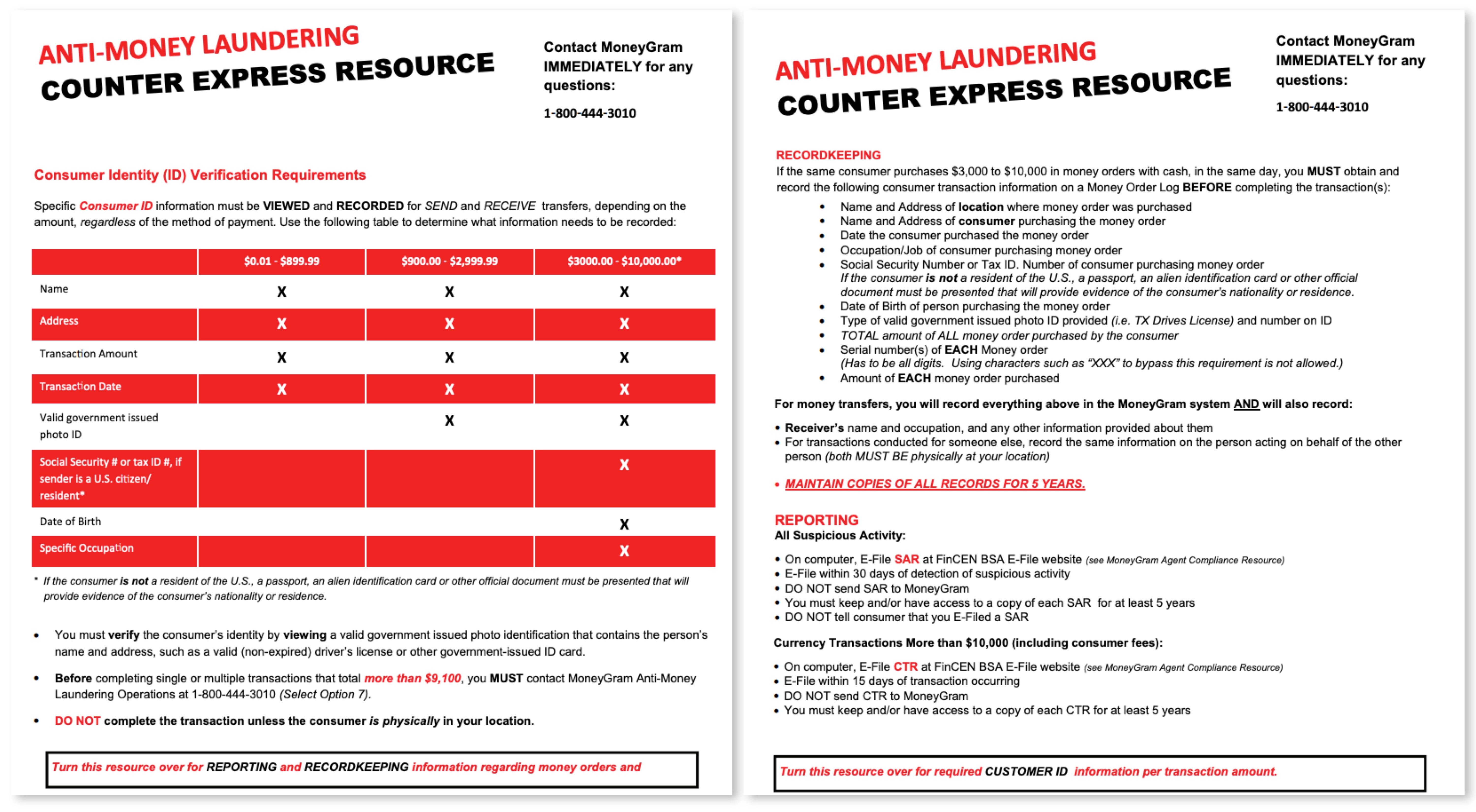

Money Services Businesses (MSB’s)—the MoneyGrams and Western Unions that dot strip malls throughout these regions—must now file Currency Transaction Reports to the federal government for any cash transaction exceeding two hundred dollars. These reports include the customer's name, address, identification information, and transaction details. The businesses must verify customers' identities before completing transactions, effectively turning each money transfer into an exercise in documentation.

It's important to note that money transfer businesses like Western Union and MoneyGram already have identification requirements for transactions—even before this new order. Western Union requires customers to present government-issued ID for in-person transactions, while MoneyGram implements a tiered approach: for transactions under $900, they record name, address, and transaction details; for $900-$2,999, they additionally require government-issued photo ID; and for $3,000-$10,000, they add requirements for Social Security numbers (for U.S. citizens/residents), date of birth, and specific occupation information.

The critical difference with the new order isn't the collection of identification—which was already happening—but what happens with that information.

Previously, this data was primarily kept within company records unless transactions exceeded $10,000 or appeared suspicious. Now, any transaction over $200 will trigger a Currency Transaction Report (CTR) that gets sent directly to FinCEN, creating a government record of routine financial activity that was previously private. These reports include detailed personal information: name, address, identification number, and transaction patterns that could potentially be analyzed for immigration enforcement purposes.

For citizens and legal residents, this represents an inconvenience and a privacy concern. For undocumented immigrants, it creates an impossible choice: cease sending financial support to family abroad or create a paper trail potentially linking them to an address in a government database—a database that immigration authorities can access.

The timing has not escaped notice.

The Treasury order was established just days before Trump considered invoking the Alien Enemies Act of 1798—a wartime authority that would dramatically expand his executive power to target and remove non-citizens. Administration officials contend the law's application will be focused on members of Tren de Aragua, a Venezuelan gang they recently designated as a foreign terrorist organization, but immigration attorneys will note the language of both the executive order and the underlying statute contains few limiting principles.

For those following Trump's policy history, the targeting of remittances represents the fulfillment of a long-standing ambition. During his campaign and early presidency, Donald Trump proposed various ideas to fund a U.S.-Mexico border wall, and one of these proposals focused on remittance flows. A Bloomberg report revealed that he had floated the possibility of using measures akin to those in the Patriot Act to curb the roughly $25.7 billion in remittances sent to Mexico in 2016, as a way to offset the wall’s costs. This idea was part of his broader rhetoric that Mexico should bear the financial burden of the wall, although it remained a speculative idea rather than a formally documented plan.

While Trump did not implement the remittance blockade during his first term due to significant legal hurdles and banking industry opposition, the current FinCEN order represents a more sophisticated approach to the same basic objective. By framing it as a targeted anti-crime measure going after drugs and cartel crime, and by using existing regulatory frameworks rather than creating new ones, the administration has found a more legally defensible path to surveilling and potentially controlling these financial flows.

Inside check-cashing businesses across the affected ZIP codes, owners are bracing for the changes to take effect. While the full impact remains to be seen, similar policies have historically led to significant drops in formal money transfer volume. When people can't send remittances through formal channels, they don't always stop sending money, they try to find alternatives. They might use informal couriers who are more expensive or less reliable, or some might attempt to carry cash themselves on a rare visit to their home country. None of these alternatives offer the security, reliability, and cost-effectiveness of formal remittance channels.

The impact could be far-reaching.

Remittances from the United States to Mexico alone totaled more than $66 billion in 2023, according to the World Bank:

The top five remittance recipient countries in 2023 are India ($125 billion), Mexico ($67 billion), China ($50 billion), the Philippines ($40 billion), and Egypt ($24 billion).

These transfers often constitute a substantial percentage of receiving countries' GDPs and provide essential support for basic necessities, education, healthcare, and small business development in communities with limited economic opportunities.

For businesses in affected ZIP codes, the new requirements create operational burdens that many small operators may find difficult to bear. Each transaction will soon trigger additional paperwork equivalent to what previously applied only to amounts fifty times larger. The reporting system may also flag submissions for being "below threshold", forcing operators to spend additional time overriding automatic systems.

As noted by journalist Barton Gellman:

Mass surveillance society subjects us all to its gaze, but not equally so. Its power touches everyone, but its hand is heaviest in communities already disadvantaged by their poverty, race, religion, ethnicity, and immigration status.

Technology and stealth allow government watchers to remain unobtrusive when they wish to be so, but their blunter tools—stop-and-frisk, suspicionless search, recruitment of snitches, compulsory questioning on intimate subjects—are conspicuous in the lives of those least empowered to object.

One particularly concerning aspect of the new order is how it might drive people to attempt "structuring": the practice of deliberately breaking up financial transactions to avoid reporting requirements. Structuring is a federal crime under the Bank Secrecy Act, punishable by up to five years in prison and substantial fines. The anti-structuring law was originally designed to catch sophisticated money launderers and drug traffickers who would break large cash deposits into smaller ones to avoid triggering the $10,000 reporting requirement.

Now, ordinary people sending remittances might unknowingly commit this crime simply by trying to maintain their financial privacy.

What makes structuring laws so pernicious is that they criminalize behavior that would otherwise be entirely legal (making smaller deposits or transfer) based solely on the intention to avoid government surveillance. This creates a thought crime where people can be prosecuted not for the act itself, but for why they did it.

A crucial point about the order is that while it specifically targets money services businesses, it doesn't apply to banks.

This creates a two-tiered system of financial surveillance that will disproportionately affect communities with limited access to traditional banking services. While both Western Union and MoneyGram offer digital options through their apps and websites, these digital services still require identity verification and often payment methods like credit cards or bank accounts that many undocumented immigrants lack. For those without such financial access, in-person services at agent locations remain the primary option, making them especially vulnerable to this expanded surveillance.

It is my opinion that this current Geographic Targeting Order could be intended to serve as a proof of concept for potential nationwide implementation. The systems and processes being developed now could be scaled up, with the infrastructure being built with expansion in mind.

Such expansion would represent a fundamentally negative shift in Americans' financial privacy.

Currently, the vast majority of everyday financial transactions occur without government notification. A national reporting threshold of $200 would effectively place most Americans' routine financial activities under potential government scrutiny. For a president who consistently positioned remittance flows as a policy lever throughout both his campaigns, first as a way to fund a border wall and now as part of a broader deportation strategy, the infrastructure being created through this "pilot program" provides an additional brick in the foundation of the nationwide implementation of policies long envisioned by the far-right, but was previously difficult to execute.

The Geographic Targeting Order's lowered reporting threshold could create another data pipeline potentially accessible through the sprawling network of fusion centers along the southwest border region. As MSB’s process newly required Currency Transaction Reports for transactions over $200, this information flows to FinCEN but could eventually reach regional intelligence centers that operate in the affected counties.

"Fusion centers enable ICE to coopt local police databases and surveillance tools that otherwise couldn't be used for deportation purposes," explains a 2024 report from the Surveillance Technology Oversight Project.

[Author’s Note: I was previously employed at S.T.O.P.]

While the specific ZIP codes targeted by the FinCEN order may not directly house fusion centers, affected areas like San Diego County and the Texas border region are served by intelligence hubs such as the San Diego Law Enforcement Coordination Center and various Texas fusion centers.

The report notes that "fusion center participants routinely give ICE sensitive data, violating state and local protections for undocumented immigrants," suggesting that even if FinCEN data isn't directly shared, fusion centers could become conduits through which financial intelligence eventually reaches immigration enforcement, creating troubling implications for immigrants in these communities who rely on money transfer services.

The FinCEN Geographic Targeting Order expires after six months unless renewed, and by law can only remain in effect for 180 days–though it can be renewed indefinitely. Previous GTOs targeting real estate transactions in specific markets have been renewed dozens of times, effectively becoming permanent fixtures.

As the new policy takes effect, residents in affected areas will need to weigh difficult choices. Some might break larger transfers into multiple transactions under the $200 threshold, but this tactic comes with significant risks. "Structuring", the deliberate splitting of transactions to avoid reporting requirements, is a federal crime under the Bank Secrecy Act, punishable by up to five years in prison and substantial fines.

MSB’s are specifically trained to identify and report such behavior.

For undocumented immigrants who already use these services with foreign passports or consular ID’s, the risk calculation has suddenly changed.

While these forms of identification were previously acceptable for the companies' internal compliance, the automatic government reporting transforms routine financial activity into potential evidence. Many remittance corridors to Latin American countries, including Mexico, Guatemala, and Honduras, already require senders to provide full address information—data that will now be transmitted to federal authorities with every transaction over $200.

This expansion of financial surveillance doesn't exist in isolation.

In fact, it is part of a broader trend of lowering reporting thresholds across multiple government agencies. In 2021, Biden’s American Rescue Plan Act included a provision to require payment apps like Venmo, PayPal, and Cash App to report aggregate annual transactions exceeding $600 to the IRS through Form 1099-K—drastically lowering the previous threshold of $20,000 and 200 transactions. While implementation of this provision was delayed until this 2025 tax year and applies only to payments for goods and services (not personal transfers or remittances), it represented another front in the expansion of financial monitoring.

In America's border communities in 2025, the act of sending money home is being transformed from a routine transaction into a documented activity with potential immigration consequences. The question now is whether this transformation will remain limited to thirty ZIP codes or whether it represents the leading edge of a new approach to financial surveillance nationwide—the culmination of a policy vision first articulated nearly a decade ago that has evolved from campaign rhetoric to administrative reality.

Bottom Line: MoneyGram, Western Union, and other MSB’s already maintain records of customer transactions for five years, as required by anti-money laundering regulations. Under the new reporting threshold, those records will now be automatically shared with the government and potentially accessible to immigration enforcement agencies, creating a database that could be mined not just for current enforcement actions but potentially for retrospective investigations of past financial activities.

Excellent work! On a separate but tightly and timely related note you should be made aware of the following high priority item: https://substack.com/@olgalautman/note/c-100390154